Today, Weeden & Co. is a venture and start-up management firm. We look for opportunities at the intersection of finance and technology. We will only invest in companies where we can leverage our knowledge and relationships to build successful and seaworthy ships in the tradition of the S. S. Marion Chilcott.

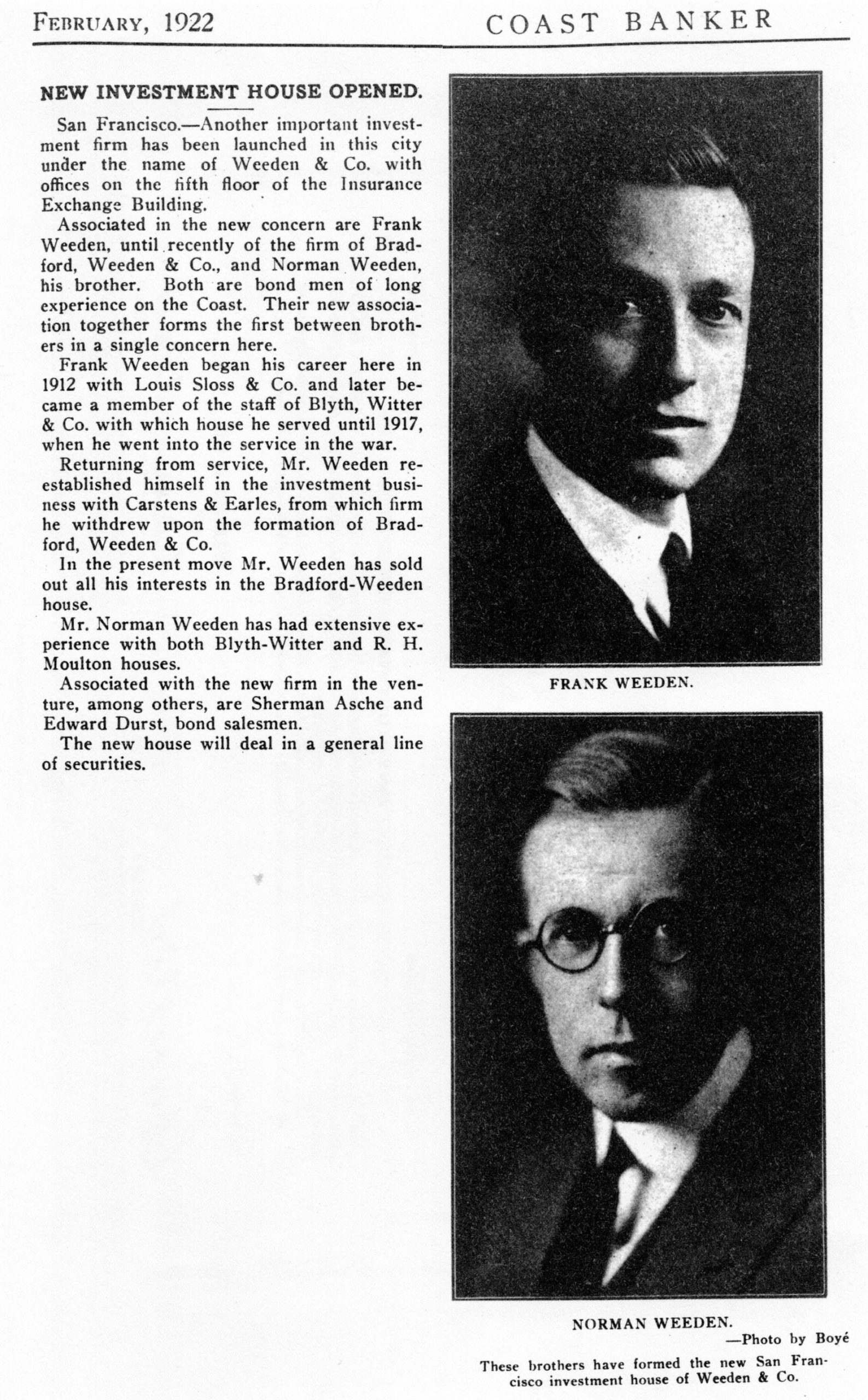

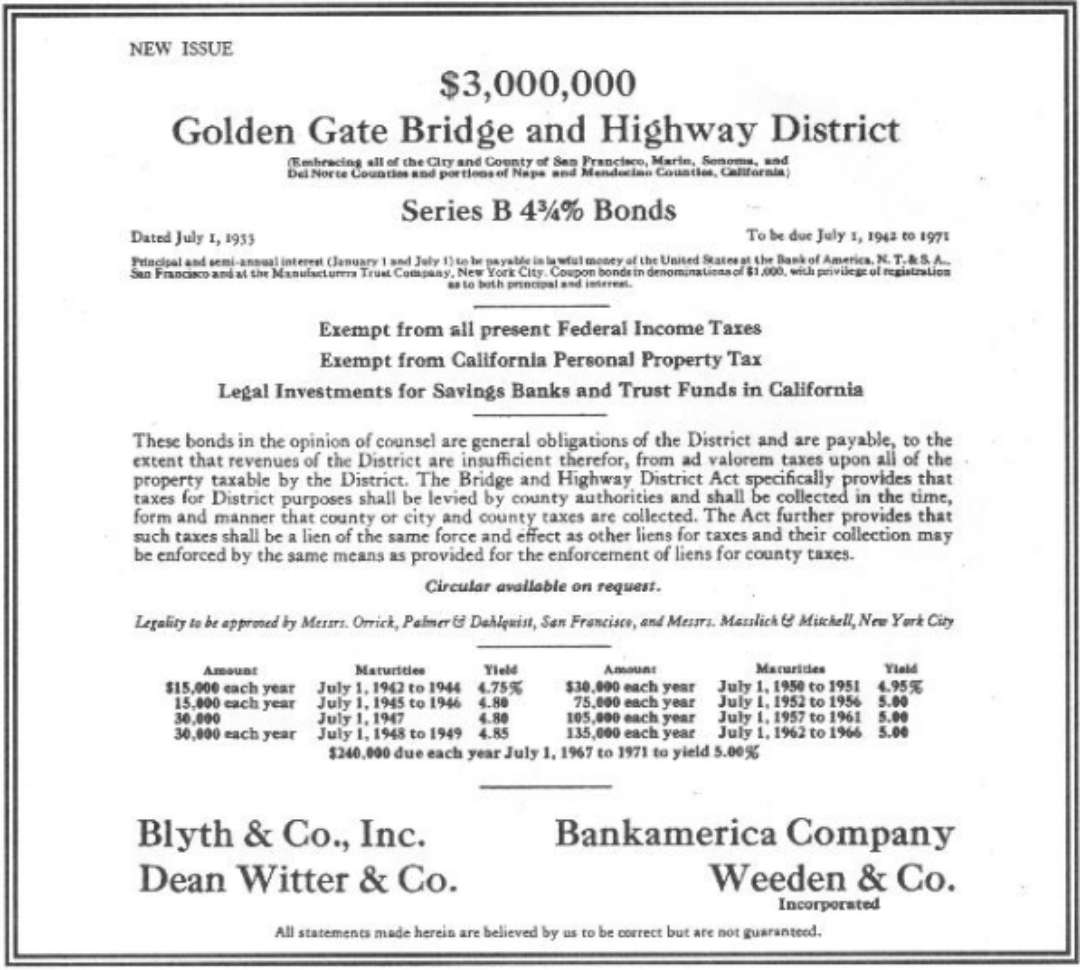

After working at the San Francisco firm of Blyth, Witter, Frank, and his brother Norman started Weeden & Co. with a $20,000 loan from their father, Captain Henry Weeden, in 1922. (Of historical interest, Blyth, Witter split up in 1924. Charles Blyth started another firm, Blyth Eastman Dillon. This firm was purchased by PaineWebber, which, in turn, was purchased by UBS. Meanwhile, Dean Witter founded his eponymous firm, which grew into the largest retail firm on the West Coast. Sears purchased Dean Witter but later sold it to Morgan Stanley. The west-coast roots of these firms continue to this day.)

Before starting Weeden, Frank often went on sales calls with Dean Witter, where the two pitched bonds to small banks in the West. On one occasion, Dean Witter said he couldn’t meet with a small bank and asked Frank to make the sales call. Dean offered, “Don’t worry if you don’t sell any bonds, as the client is one tough and ornery customer.” Frank took the ferry to Marin Co. and walked into the bank with a briefcase of bonds. “I’m sure, sir, you know much more about these bonds than I do. Please take a look to see if anything might interest you.” The customer scrutinizes Frank and the bonds, then comments, “Young man, your approach is a welcome change from the other salesmen telling me what I should buy.” The customer buys the entire briefcase of bonds, and Dean is stunned as Frank returns with a very large check.

Frank and Norman ran Weeden on a shoestring with nary a white shoe to be found. Weeden & Co. was profitable from the onset and stayed so through the Great Depression. For instance, Frank had to rush bonds to a client. He handed the messenger a one-way subway token. The messenger asked Frank for the return fare, to which Frank replied, “There’s only a rush to deliver the bonds.”

Frank ran Weeden, but it was more of an understanding than discipline. At one point, one of the traders began to drink at lunch, and Frank needed to act. Frank asked the trader to join him for a walk around the block. But Frank could not bring himself to fire him, so they kept circling the block. The trader, then realizing the reason for the walk and Frank’s unease, appreciated what became his second chance. He never drank again during trading hours.

The financial industry’s structure was important to Frank, who became involved in committees after the Great Depression. In September 1937, Frank joined the Investment Bankers Code Committee. Frank and the committee decided on guidelines that focused on standards and principles rather than details. For instance, they recommended that the institution’s capacity be disclosed to the customer while placing an order, whether as an agent or principal. Frank spoke for the committee:

“In the last analysis, we are going to be judged and regulated according to whether or not we serve a proper function. I am inclined to think that in the past about the only excuse for many houses being in business was the fact that they were making a profit. Now we are being analyzed not alone by the Securities and Exchange Commission but by the public at large and the politicians in Washington as to whether we perform a necessary function.”

The Investment Bankers Code Committee also recommended that the industry self-regulate. From this committee emerged the National Association of Security Dealers (“NASD”), which regulated the firms that were not members of the NYSE. NASD eventually becomes FINRA.

In 1967, Alan, Jack, and Don Weeden, Frank’s sons, staged an intrafamilial mutiny. They presented the Weeden Board with an ultimatum: either Frank step down as president, or the troika would leave the firm. They believed Frank’s frugality and old-style management style restricted the firm’s growth during the frothy late ’60s. Alan became president, Don took control of stock trading, and Jack ran the back office.

Events from 1967 to 1978 are well documented in Don’s book, Weeden & Co. The New York Stock Exchange and the Struggle Over a National Securities Market, and a lead Institutional Investor article, The Tragedy of Don Weeden, June 1978. During the decade between 1967 and 1977, the new management grew staff, greatly increased overhead, and made two acquisitions, Wainwright Securities and W.H. Reeves. Wainwright was shut down within 5 months at a loss of millions and W.H. Reeves bought their firm back. The combination of increased overhead, acquistions and reduced profit margins from negotiated commissions sealed Weeden’s fate.

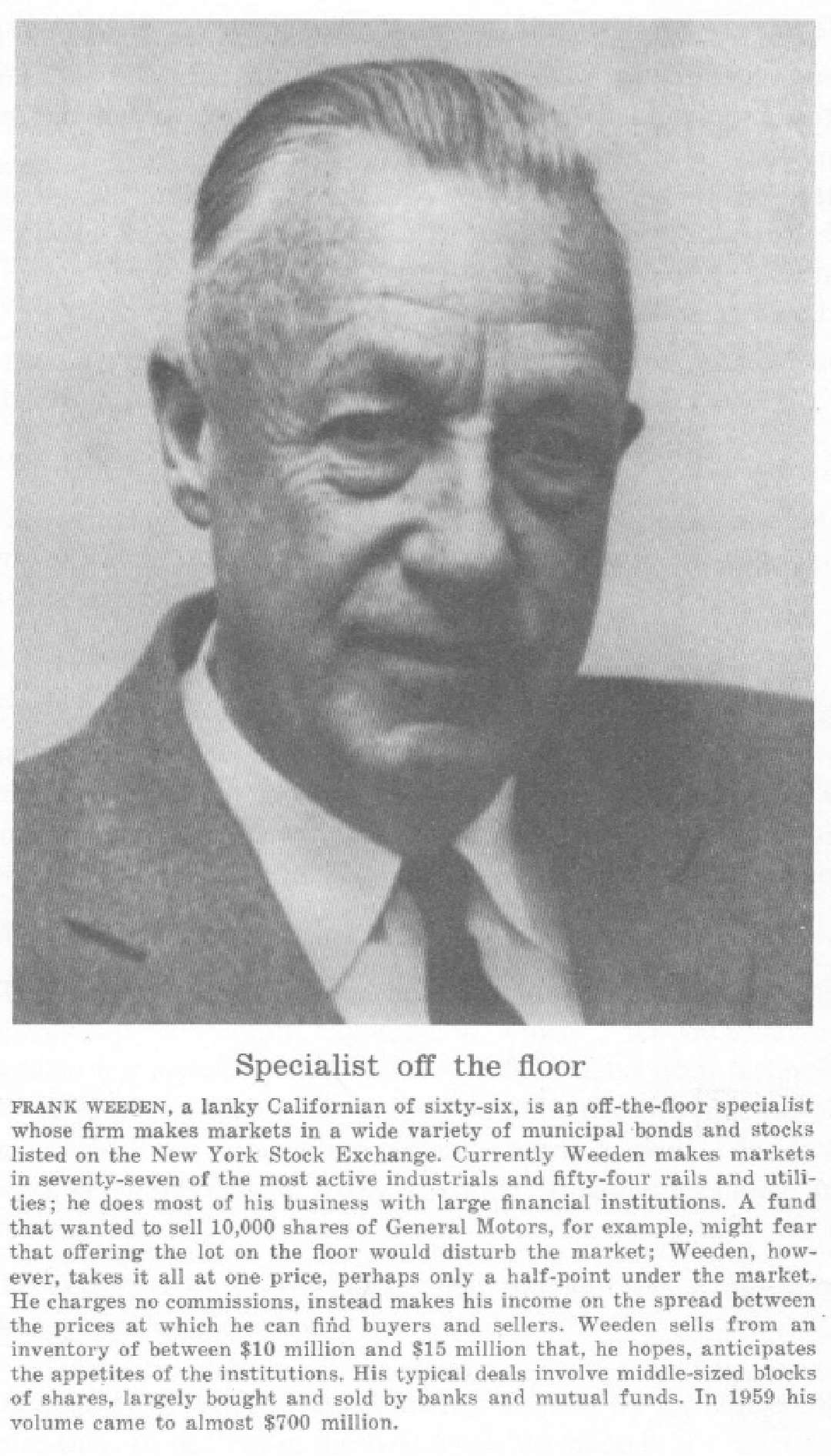

In 1974, I started at Weeden to help program a system called the Automated System for Trading (AST). Frank always called it a half-AST system, but AST was, in fact, Frank’s baby. AST brought efficiency to Weeden’s trading operations, which the old tar thoroughly embraced. Operators on the trading desks entered trades directly into the system, and inventories, profits, and capital risk were immediately updated. The AST was the first real-time inventory management system on Wall Street and greatly interested many major trading firms. Our software team was led by Jeremy Connelly, a great first boss who would interrupt a meeting on complex software design to declaim on Swann’s Way.

Though a rookie, I got to work directly with Frank, who, without management responsibilities, focused his energies on the AST system. Frank endlessly came up with features to improve the efficiency of trading and sales. We developed software to provide real-time bid/ask prices for bonds and a monitoring system to alert sales teams of trading opportunities. While working to integrate AST with Quotron, Frank was offered the opportunity to purchase a large block of Quotron stock, resulting in Frank becoming Quotron’s largest shareholder.

During these years, Don and Jack were very active in fighting the New York Stock Exchange, which considered the upstairs, or Third Market, competition with the floor. The industry had continual discussions about market structure, and the SEC established the National Market Advisory Board (“NMAB”) in 1975 to explore the advantages of different platforms. Don was a big proponent of an industry-wide CLOB (Central Limit Order Book), enabling an open order book and a level playing field for trading. To prove the viability of such a system, Don and Jack decided to reassign the AST programming team to a new system called WHAM (Weeden Holding Automated Market). Frank strongly opposed this reallocation, as he knew Weeden’s survival depended more on trading efficiencies than on convincing the industry to change.

As losses hit Weeden, Don took over in 1977, but by then, Weeden had exhausted most of its accumulated capital and had a net capital deficit. Don fought hard to cut personnel and offices, but revenues dropped faster than costs. Unqualified, I was promoted to Vice President of IT one morning and told to lay off five keypunch operators by afternoon. Weeden was now, sadly, a sinking ship. Amid the flotsam and jetsam, I negotiated the giveaway of the WHAM system to Peter Madoff, Bernie’s younger brother. Don, in a final desperate effort, asked Frank to provide sufficient capital to keep the firm afloat, but Frank deferred, saying that he preferred to retain his stakes in Quotron, Instinet, and other investments.

Weeden was forced into a merger with Moseley, Hallgarten, at which point Frank purchased the AST system and set up QV Trading Systems. As an independent company, QV signed up trading firms such as Nomura, Wertheim, PaineWebber, Smith NewCourt, UBS, Drexel Burnham, and even the New York Stock Exchange. Frank passed away in 1984, and most of QV’s ownership was transferred to the Frank Weeden Foundation, run by Alan Weeden. I objected to this transition and left QV to start Document Technologies (“dTech”), which developed software for the SEC’s new EDGAR system. Our software, EDGAREase, quickly became the leading software tool for filing electronic financial documents with the Commission.